Systems and methods for funds transfer account aggregator

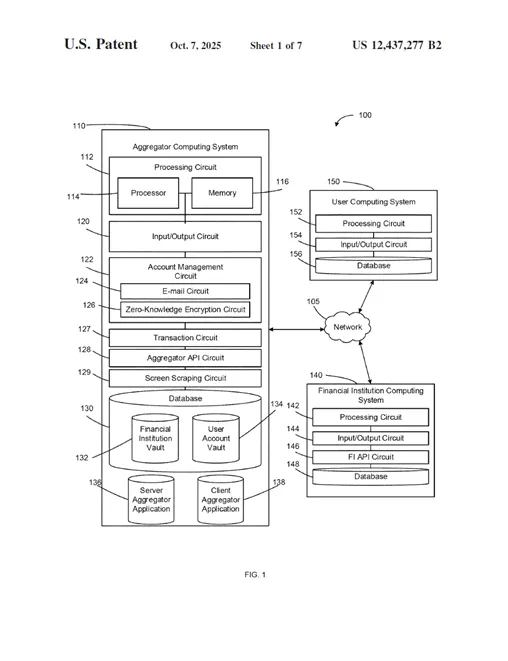

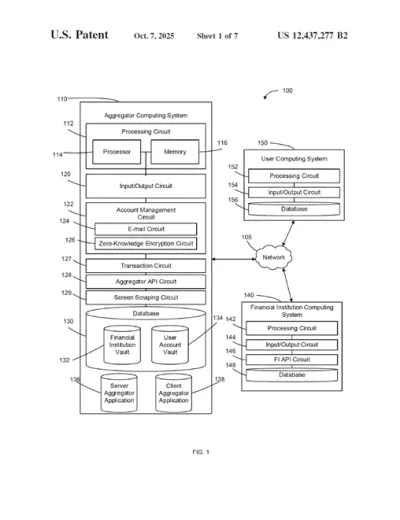

Systems and methods for a computing system for facilitating financial transactions are provided. The system is structured to aggregate user data including sender data and recipient data, and to facilitate creating and aggregating user accounts at multiple financial institutions. The system includes an account management circuit structured to generate a user account, an executable structured to determine whether a user browser has navigated to a first hyperlink, and a transaction circuit structured to facilitate a transaction. Specifically, the transaction circuit is structured to receive an indication that the user browser has accessed the first hyperlink, determine whether a first financial institution account exists, facilitate a financial transaction, and generate a notification including a confirmation that the transaction was completed.

[Migrant Economy]

Despite huge volumes sent, Immigrants experience high fees and poor financial connection to their home countries as the financial institutions do not have required access to their financial data

[Cross-Border payment Collections]

International card processing is unstable across emerging markets.

Collections via non-card payment methods offer a poor experience across emerging markets with PayPal the dominant option

[Gig Economy]

Remote workers across emerging markets have limited access to financial services due to a lack of financial data

Payment Initiation Service (PIS)

Solutions for Neobanks & Fintechs

Account Information Service (AIS)

Solutions for Neobanks & Fintechs

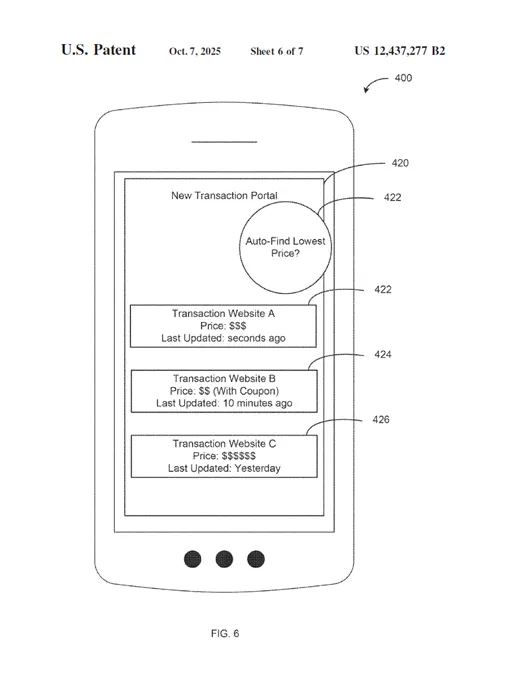

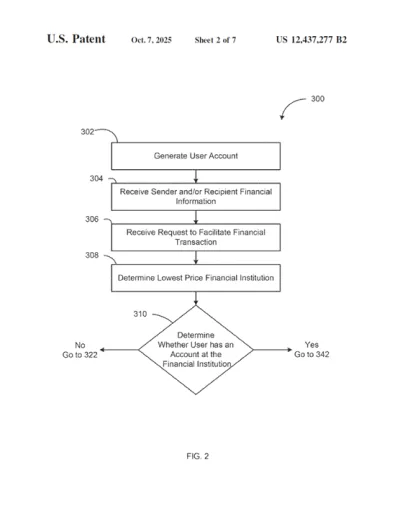

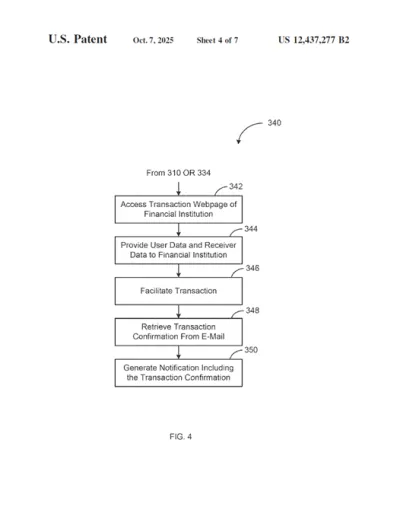

Financial institutions such as banks, credit unions, and the likes, may provide funds transfer services. The funds transfer services may include transactions such as sending money to a recipient, sending money to a recipient in a different currency, sending money to a recipient in a different country, making a payment, and the likes.

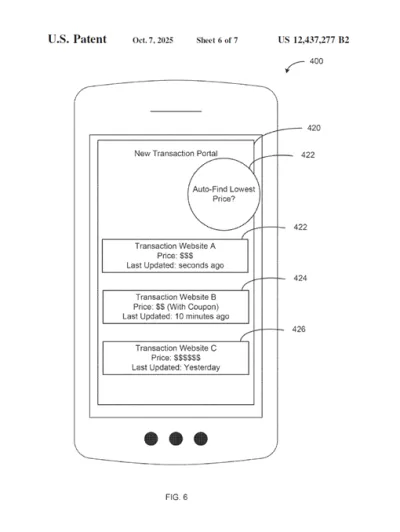

The financial institutions may charge a fee for each of these transactions. The fee may change frequently and/or be based on a recipient location, time of day, and other parameters. Accordingly, it may be desirable to use the services of the lowest cost financial institution.

This technology has been designed to enable customers across the Ideal Customer Profiles below explore price-driven sensitivity and decisioning

AIS & PIS can facilitate the transfer of Immigrants’ financial data across financial institutions in emerging markets- an industry/market first.

Initiate international money transfers on remittance apps from a third-party application (PIS)

Obtain financial data of international money transfers made on remittance apps (AIS)

SYSTEMS AND METHODS FOR FUNDS TRANSFER ACCOUNT AGGREGATOR

Immigrants experience poor financial connection to their home countries as the financial institutions do not have required access to their financial data

This technology has been designed to enable customers across the Ideal Customer Profiles below explore price-driven sensitivity and decisioning

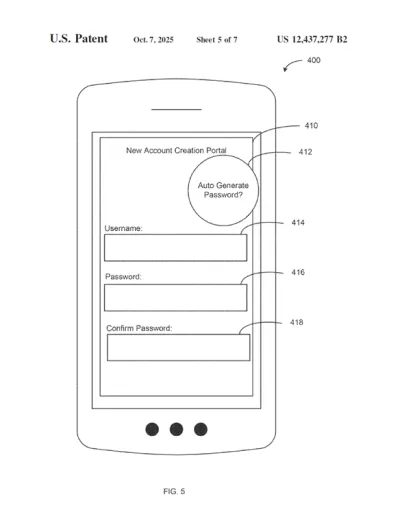

The system is structured to aggregate user data including sender data and recipient data, and to facilitate creating and aggregating user accounts at multiple financial institutions.

The system includes an account management circuit structured to generate a user account, an executable structured to determine whether a user browser has navigated to a first hyperlink, and a transaction circuit structured to facilitate a transaction. Specifically, the transaction circuit is structured to receive an indication that the user browser has accessed the first hyperlink, determine whether a first financial institution account exists, facilitate a financial transaction, and generate a notification including a confirmation that the transaction was completed.

Industries where the invention can be useful?

Financial Institutions (Commercial Banks, Credit Unions, Insurance Companies, Microfinance Banks, Savings & Loans Associations, Pension Funds, Mortgage Companies, Investment Banks & Brokers) Mobile Money Operators Money Transmitters/Remittance Companies Card Schemes Open-source financial Ecosystems Payment Service Providers Non-Banking Financial Companies Telcos Financial Services MarketplacesAn estimate of the total addressable market?

[Gig Economy] The market was valued at around $557-$561 billion in 2024/2025. Forecasts indicate it will exceed $1.8 trillion by 2032–2033. [Migrant Economy] Remittances (Funds sent home): Global remittance flows to low- and middle-income countries were estimated to reach USD 656 billion in 2023. Total global remittances (including high-income countries) were estimated at USD 857 billion in 2023 and projected to rise to over USD 900 billion in 2024. [Cross-border payment collections] Retail/non-wholesale (B2B, B2C, C2B, C2C): This segment is growing rapidly, with a total value of $39.9 trillion in 2024, expected to reach $64.5 trillion by 2032.Potential Customers/End Users. Who might benefit?

Financial Institutions (Commercial Banks, Credit Unions, Insurance Companies, Microfinance Banks, Savings & Loans Associations, Pension Funds, Mortgage Companies, Investment Banks & Brokers) Mobile Money Operators Money Transmitters/Remittance Companies Card Schemes Open-source financial Ecosystems Payment Service Providers Non-Banking Financial Companies Telcos Financial Services MarketplacesDocuments

-

1770725156470_847.pdf

Actions

Added all portfolio

| Country | Current Status | Patent Application Number | Patent Number | Applicant / Current Assignee Name | Title | Google Patent Link |

| USA | Granted | 18/277,971 | US 12,437,277B2 | KAOSHI INC., Chicago,IL(US) | SYSTEMS AND METHODS FOR FUNDS TRANSFER ACCOUNT AGGREGATOR | Google patent link |

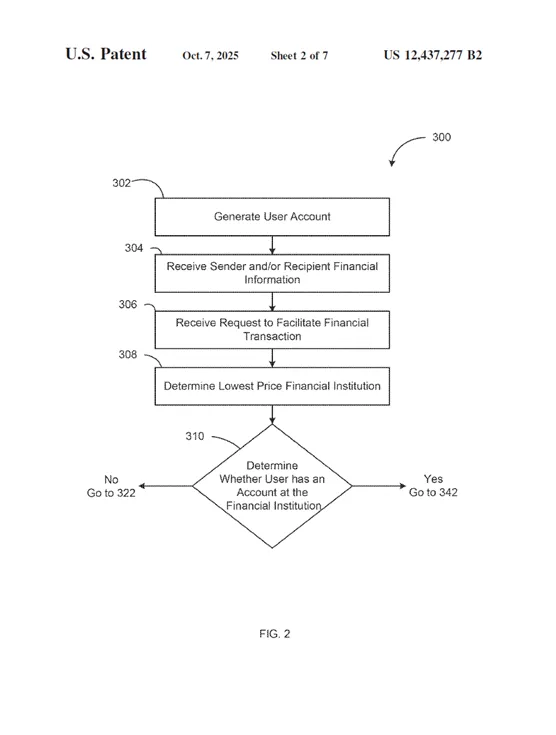

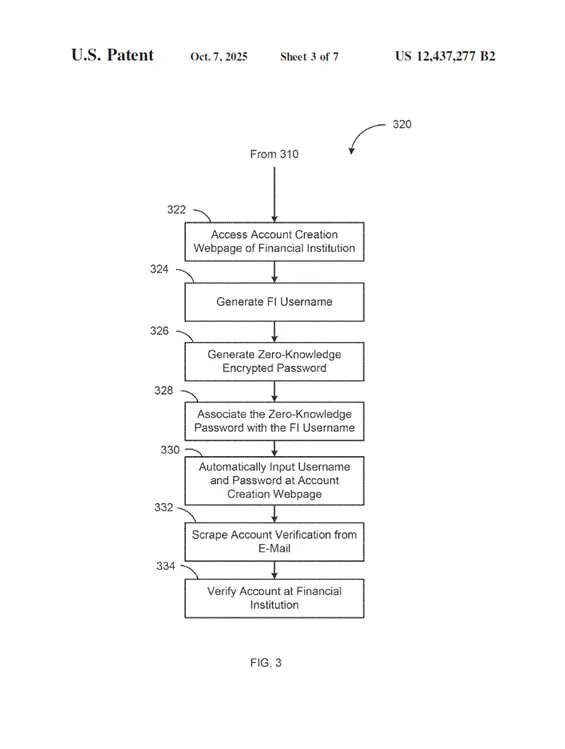

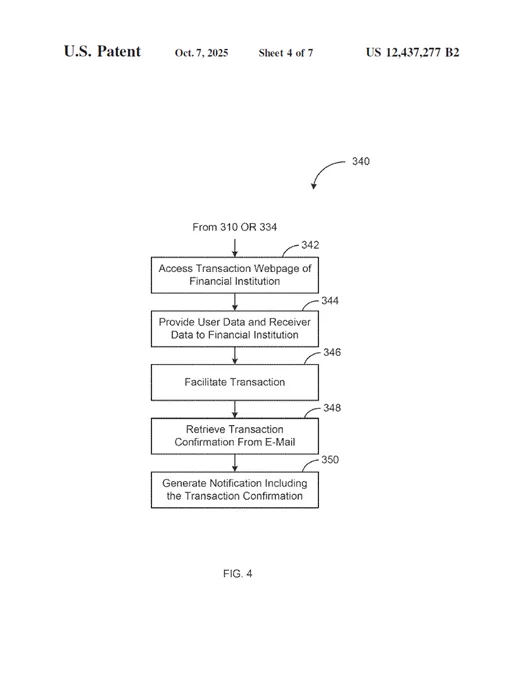

You may also like the following patent